The Emergency Fund

Are you ready for your money to start taking care of you?

If so, then this is where safety begins: the Emergency Fund.

It's devastating when I see how many families have little or no savings protecting them from misfortune. Just how bad is it? In June of 2015, Bankrate's "Financial Security Index" survey reported that 29 percent of Americans — almost 1 in 3 — had no emergency savings. A mere 22 percent said they had enough savings to cover six months' worth of expenses. About 21 percent said they had some savings, but less than three months' worth.

Want more? The 2014 Survey of Household Economics and Decisionmaking [PDF], as published by the Federal Reserve Board in 2015, found that 47 percent of respondents could not cover a $400 emergency expense without selling something or borrowing money. Only 45 percent of people surveyed said they had enough savings to cover three months' worth of expenses.

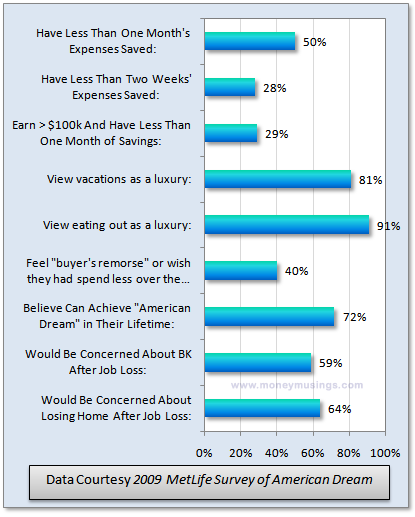

(For those who'd like to see some older data, here's my chart summarizing a 2009 MetLife savings survey.)

{kind=link}

Look: Your debt payoff plan is about getting yourself out of debt now, and doing it as quickly as possible.

Your Emergency Fund, on the other hand, is about staying out of debt. It's the force-field you build around your life. It's there to keep the debt ghoulies out.

And quite a force-field it is. A fully-funded Emergency Fund means freeing yourself from debt forever.

Pause for an ... Essay?

Yeah, that's right. A short essay. Because it's worth reading.

Perhaps the best essay I've yet read on the topic of savings is "Saving for Greatness," as published on the internet by a fellow named Luther Setzer. Mr. Setzer admits that he didn't write the essay — that he simply saw it in a financial pamphlet and thought it needed to be repeated elsewhere. I highly recommend that you take a moment to read this piece. It's short on length, but heavy on inspiration. And meaning. It sets the stage for everything else I discuss on this page.

And now that I have some savings to my name, I can attest to the truth of this anonymous author's work.

Greatness, indeed.

Ready for Emergencies: How Much Should I Save?

Whether you call it an "Emergency Fund" (Dave Ramsey), "Contingency Fund" (Jerrold Mundis and Mary Hunt), or "Safe and Sound Money" (Suze Orman), there is no one-size-fits-all here. Rather, the amount you keep in your E-fund must be an amount that makes sense for you. It will depend on whether you're already debt-free ... or loaded down with debt. It will depend on whether you have a single- or dual-income household. It will depend on what makes you feel secure.

If you're smack in the middle of a messy debt paydown, for instance, it doesn't (usually) make much sense to keep a big pile of cash in savings. Why on earth would you want to clutch at money that earns you, say, 1 percent interest, when your balance sheet is clogged with debt that's costing you 10 ... 12 ... 15 percent or more? You're sending money straight out the front door.

Yet lots of people do just that. The reasoning is easy enough: Having a chunk of cash in savings helps you feel secure. But if you're also carrying expensive debt (read: any interest-accruing debt other than perhaps mortgage debt), then that "security" you feel when you check your savings balances is largely an illusion.

But families do have a need for some savings behind them, whether they're in debt or not. If you're going to break the cycle of credit-card dependence, after all, you will need to have some money available for life's little emergencies. Otherwise you'll turn to plastic again and again. You'll be just as dependent upon it as you ever were.

What you need is a "beginner" Emergency Fund.

The Beginner Emergency Fund

When it comes to "beginner" Emergency Funds, many people have found success with Dave Ramsey's approach. I, too, am an advocate of his methodology.

In his "Baby Steps" plan, Ramsey advocates that folks start with an Emergency Fund of only $1,000. (Or $500 if you make $20,000 or less per year.) You should keep this amount in your Emergency Fund, and no more, until all your debts — other than your mortgage, if you have one — are paid off.

Ramsey isn't alone in this idea of a starter Emergency Fund. Fellow author David Bach, in his 2004 book The Automatic Millionaire, recommends something similar: Build an emergency fund of one month's worth of expenses before embarking on any sort of debt payoff plan.

The Full-Strength Emergency Fund

Once you're debt-free, Ramsey and Bach suggest the same time-tested goal as do most financial advisors:

Build a permanent savings cushion of 3 to 6 months' worth of living expenses.Financial-advice queen Suze Orman goes a step further:

"Conventional wisdom says one should have three to six months' worth of living expenses set aside in a safe place, and, for the most part, I agree with this," she wrote in The Courage to Be Rich in 2002. A year later, though, she rethought her stance.

"I want you to have at least eight months of cash saved," she told readers in 2003's The Laws of Money, The Lessons of Life. "I no longer believe that the three- to six-month time frame that has been traditionally recommended as a reserve fund is enough."

And something else Orman wrote in Courage to Be Rich bears repeating. "There is no set formula for 'safe and sound' money, because your relationship with your money is personal and unique to you. So you need to ask yourself this question: How much money do I want to have safe and sound for an emergency?"

Let the voice in your head answer that. If you're married, let your spouse offer an answer, too.

Decide what will make you feel the most secure. And then get to saving.

Where to Keep Your Savings

Another popular question: Where will I keep my Emergency Fund?

This question is more important than you might imagine. If your Emergency Fund is too easy to access, you might be tempted to dip into it for things that are ... well, not emergencies.

At the same time, though, it needs to be liquid (easily convertible to cash) and kept somewhere that allows fairly prompt access. After all, they call them "emergencies" for a reason.

So make an assessment of the banking and brokerage resources available to you. You'll want the account to:

- Pay decent interest,

- Be devoid of fees,

- Not be too easy to access, and

- Not be too difficult to access.

A money-market account at a bank across town, or at a brokerage, might be the right fit. Perhaps a second savings account (usually not attached to a checking account) at your credit union or bank would work.

Or you could do what many, many savers are now doing: store your money at online-accessible banks like Capital One 360 and a host of others (see "Related Articles" below). Savings deposited in these institutions have historically paid much better interest than most other savings accounts, for one thing. Their minimum initial deposits are typically either very low ($25) or zero, and there are no fees.

But most importantly: Access to your money is restricted ... just a little. Once you make a transfer request, the funds generally can be wired into your current checking account and available within two working days.

Get That E-Fund Going!

There are basically three ways to come up with the money for your emergency fund, no matter whether it's of the "beginner" or "full-fledged" variety:

(1) Earn more money. Work more hours. Take on a part-time job. Use a Spending Plan, and direct all extra money to savings.

(2) Spend less money. Use a Spending Plan, and direct all extra money to savings.

(3) Sell stuff. Direct all proceeds to savings.

You know what? Some folks have even been crazy enough to engage in wild combinations of those three actions. It's insane, I know. But worth it.

As Laura Bruce notes in her excellent Bankrate.com article "How to Build Your Emergency Fund," people who have never been able to get e-funds together in the past can have consistent success once they begin treating their e-fund contribution as a monthly bill.

"Putting money aside on your own is hard," she writes. "Retirement plans are successful because the money comes out of your paycheck before you can get your hands on it and because there are taxes and penalties for early withdrawals. But stashing money in an easy-access money market account takes discipline."

What are you willing to do for some security in your life? What are you willing to sacrifice now in return for greatly lessened financial stress in the future?

And why would you let anything hold you back?

Afterword: More Authors' Thoughts

What do you do when your car breaks down in the morning, your wife calls later to tell you the dog ate the sofa, you lose your biggest account in the afternoon, and when you get home in the evening you find a note from the plumber saying he replaced the living room baseboard, and P.S., your furnace is dead? You express deep gratitude for your contingency fund, that's what.

— Jerrold Mundis, How to Get Out of Debt, Stay Out of Debt, and Live Prosperously

Maybe you've felt it. The rush in the pit of your stomach when you hear the pinging sound in your car, and you wonder how you'll ever pay the mechanic. The tightness in your chest when the plumber tells you it will be $185 to fix the shower. The rock-hard knots in your back when you realize that the check you mailed to the electric company will probably bounce.

These are the feelings of not having any Savings. And when you start to save — when you really sock it away, month after month — these feelings stop. You can put these feelings in a box and mail them to the moon, because they won't be with you anymore.

— Elizabeth Warren and Amelia Tyagi, All Your Worth

The basic truth is that you must plan for the unexpected, because it will happen. Although we don't know what form it will take, it will come. Cars do break; women do get pregnant; people do get hurt or die; businesses do lay people off. To think otherwise is naive. So you have to plan for it. Saving into an emergency fund is an essential element for financial peace.

— Dave Ramsey, Financial Peace Revisited

You start the emergency fund with $1,000, but a fully-funded emergency fund will usually range from $5,000 to $25,000. The typical family that can make it on $3,000 per month might have a $10,000 emergency fund as a minimum. What would it feel like to have no payments but the house, and $10,000 in savings for when it rains?

Remember what we said about emergencies a couple of chapters back? It will rain; you need an umbrella. When the big stuff happens, like the job layoff or the blown car engine, you can't depend on credit cards. If you use debt to cover emergencies, you have backtracked again. A well-designed Total Money Makeover will walk you out of debt forever. A strong foundation in your financial house includes the big savings account, which will be used just for emergencies.

— Dave Ramsey, The Total Money Makeover

The amount you need in your emergency fund is not the same as what you earn in three to six months. It's also not what you typically spend. When you're working, you spend much more freely than you would if you were just trying to get by.

— Jean Chatzky, You Don't Have to Be Rich

Why bother to become a better saver? Because boosting your saving prowess can have a huge emotional payoff. Nine out of ten savers say they're 'happy' with their lives. Savers are more likely than spenders to be happy with their lifestyle, self-esteem, even their weight and appearance. They're more likely to feel confident and content, less likely to feel stressed and restless. Spenders are just the opposite: They're more likely to be frustrated with their lot in life.

— Jean Chatzky, You Don't Have to Be Rich (2003)

Small steps are inevitably going to be your first steps, and they definitely count. Once you have put aside $25 one week and discovered that you can live in fact without that $25 in your spending account, then you have the confidence to know that you can do it again. You may even have the confidence to think, "Well, hey, if I put aside $25 and I didn't miss it, I'm going to try to put $50 aside and not miss it. — Jean Chatzky, Bankrate.com Interview, 2007-07-23

You need to understand and know that the main unknown in your financial life — and where most people tend to get in trouble with their money — is when something happens that you are not expecting. A job loss, an accident, a family crisis, an illness (either your own or that of a parent or child), a death or disability, or an unexpected divorce — each is an unforeseen even that affects your expenses and finances. When an unforeseen event does occur, your biggest problem usually will be to know where to get the money you need to pay for your known expenses and your unknown, unanticipated ones until you can become safe and secure again. Keep in mind that your financial world can be shaken or destroyed by very common, unforeseen possiblilties. This has always been the case, of course — and in a time of economic and global uncertainty, it is especially true. People who sail through difficulties with relatively little financial harm do so because they have prepared for them.

— Suze Orman, The Laws of Money, The Lessons of Life

Another problem that you may encounter in preparing for the unknown is that you find it hard to save — and can't imagine setting up an account with eight months worth of expenses in a short amount of time. Well, my friend, if this is the case, the way for you to create an emergency fund is simply to take every extra penny you have, put it into a money market account, and save it there. You have to make a decision here. Which means more to you — having a Starbucks coffee this afternoon and going to the movies tonight, or knowing that you and your loved ones will be protected even if you lose your job or get sick? Doing what is right for you — including making sure you'll have what you need in any sitution — may mean giving up what you want right now to pay for what you could need later on. I hope you decide to do this, for you'll be amazed at how much control over your life you will feel with your emergency fund standing behind you.

— Suze Orman, The Laws of Money, The Lessons of Life